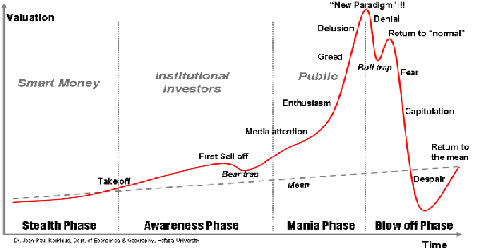

Market Cycles

THE MARKET CYCLE

The economy is cyclical, and the stock market tracks with that cycle.

This is driven by a profit cycle for the companies, compounded by the psychology of

investors. Greed and fear are very strong motivating forces affecting investor behavior.

As conditions improve, investors become increasingly confident and bid up the price of stock

relative to the fundamentals of earnings and revenues. Eventually their exuberance causes

prices to become abnormally high. A market top is reached as everyone piles in.

As the economy slows, in its normal cycle progression, corporate profits begin to stall and

decline. As these conditions deteriorate, the wise investors sell off their stocks, and prices

start to slip. A few months later, the economy will go into recession, and investors will rush to

sell before things get worse.

Soon there is panic selling, driving prices to extreme lows, as the crowd fearfully sells to

escape the end of the world. This creates a market bottom, and a fabulous buying

opportunity, as stocks quickly bounce back from this moment of despair.

The following chart illustrates the nature of a typical cycle, and the investor psychology at

the various stages:

The economy is cyclical, and the stock market tracks with that cycle.

This is driven by a profit cycle for the companies, compounded by the psychology of

investors. Greed and fear are very strong motivating forces affecting investor behavior.

As conditions improve, investors become increasingly confident and bid up the price of stock

relative to the fundamentals of earnings and revenues. Eventually their exuberance causes

prices to become abnormally high. A market top is reached as everyone piles in.

As the economy slows, in its normal cycle progression, corporate profits begin to stall and

decline. As these conditions deteriorate, the wise investors sell off their stocks, and prices

start to slip. A few months later, the economy will go into recession, and investors will rush to

sell before things get worse.

Soon there is panic selling, driving prices to extreme lows, as the crowd fearfully sells to

escape the end of the world. This creates a market bottom, and a fabulous buying

opportunity, as stocks quickly bounce back from this moment of despair.

The following chart illustrates the nature of a typical cycle, and the investor psychology at

the various stages:

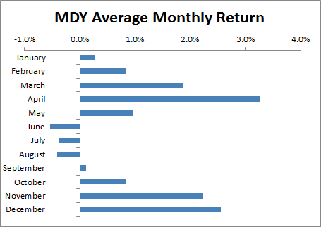

SEASONALITY

The stock market has significant seasonality. This is particularly true for the stocks of

smaller and mid-cap companies. Performance can be enhanced by seasonal timing of

purchases and sales. The old saying "sell in May and go away" can be of value, as

illustrated by the MDY (mid-cap portfolio) below:

The stock market has significant seasonality. This is particularly true for the stocks of

smaller and mid-cap companies. Performance can be enhanced by seasonal timing of

purchases and sales. The old saying "sell in May and go away" can be of value, as

illustrated by the MDY (mid-cap portfolio) below:

Large companies have much less seasonality to

their stock prices. They have only one month

that has on average been negative.

their stock prices. They have only one month

that has on average been negative.

Financial company stocks lead the market (up & down). Financial firms are the canaries in the mine shaft, and the laggards are

the capital-goods companies.

In a weakening economy, companies that sell staples outperform. Cambell Soup, Molson Coors Brewing, Colgate-Palmolive,

Coca-Cola, Altrie Group, Johnson & Johnson. Drug companies usually do well in recessions. Other stable companies include H &

R Block, Corrections Corp of America, & Service Corp International (funeral homes). Banks usually do poorly.

the capital-goods companies.

In a weakening economy, companies that sell staples outperform. Cambell Soup, Molson Coors Brewing, Colgate-Palmolive,

Coca-Cola, Altrie Group, Johnson & Johnson. Drug companies usually do well in recessions. Other stable companies include H &

R Block, Corrections Corp of America, & Service Corp International (funeral homes). Banks usually do poorly.

Business Cycle & Stock Performance

Excerpted From Fidelity Investments

Business Cycle Basics

By examining empirical evidence, the investor can attempt to create a framework for viewing present and future events

as they unfold. There are two key questions the investor may want to ask:

1. Will the historic pattern hold, or will it be altered? To answer that, you'll need to ascertain whether the factors driving

today's market are fundamentally unchanged, or whether the situation has evolved incrementally or even been radically

changed.

2. Has the market already taken the anticipated future events into account? If the factors driving the industry are the

traditional cyclical ones, the market usually will have taken them into account, because they are expected. If the factors

represent a new element in the equation, then the market may not be expecting them and may not have adjusted

accordingly.

Business Cycle and Relative Stock Performance

The following chart shows a typical business cycle and the points at which various economic sectors tend to

outperform the broader market. Click any number in the chart to learn about the cyclical characteristics of a particular

industry.

<Chart Missing>

The chart above shows a typical business cycle and the points at which various economic sectors tend to outperform

the broader market. Please note that the chart should be used for illustrative purposes only. The chart is a historical

representation of stock performance movements relative to the business cycle and is not intended to convey any

current or future economic outlook. Choose a Sector for a detail description of its role in the business cycle.

Source: 2000, Standard and Poor's, a division of McGraw-Hill Companies, based on a study analyzing the differences

in market returns of 90 Industries vs the S&P 500 during 10 complete economic cycles from December 1945 -

December 1995.

1. Consumer Non-Cyclicals

Stocks in consumer non-cyclicals (food) and consumer growth industries (cosmetics, tobacco, beverages) tend to

experience fairly steady demand and are less sensitive to changes in the business cycle. These stocks typically attract

investors when the economic cycle or bull market has matured, or is in the early stages of contraction.

2. Consumer Cyclicals (durable & non-durable)

Stocks in this category include durables and non-durables that are sensitive to interest rates as well as the business

cycle. Investors typically seek them out when the economy is in the late stages of contraction.

3. Healthcare

In general, stocks in this sector move similarly to consumer non-cyclicals. This sector is considered defensive,

meaning companies in this sector are generally unaffected by economic fluctuations. The healthcare industry consists

of pharmaceutical firms, HMOs, biotechnology firms and medical equipment suppliers. Pharmaceutical companies

are affected by competitive market shares, the pace of FDA approvals, patent lives, and the strength of the R&D

pipelines. Many biotechnology firms are still in the development stage with their fortunes largely determined by investor

perceptions of the relative merits of their R&D pipelines. With future new financing likely to be more difficult to obtain

than in the past, strategic alliances between major drug companies and biotech firms are expected to increase.

4. Financials

Stocks in housing-related industries tend to respond well to falling interest rates and are often targeted by investors in

the mid to late stages of an economic contraction. Non-mortgage-dependent banks are generally driven by commercial

and consumer loan growth, and tend to be favored by investors during the middle of the cycle.

5. Technology

Technology stocks can be cyclical to the degree that they depend on capital spending and business or consumer

demand. However, they may also have long-term growth potential as technological products find broader applications

and as new technologies are developed. Technology stocks are usually popular during early to mid stages of an

economic expansion.

6. Basic Industry

Profits of basic industries are driven by high utilization of capacity and strong market demand for products. Therefore,

their stocks tend to be popular with investors late in an economic expansion. For basic material companies, the global

economic picture and supply/demand equation also affect stock price movements.

7. Capital Goods

Capital spending tends to increase midway through the business cycle, as the economy is heating up and higher

demand for products leads companies to expand their production capacity. Demand in global export markets is key for

agricultural equipment, industrial machinery, and machine tools.

8. Transportation

Railroads and other surface carriers tend to react early to a pickup in the economy. Airlines are subject to cyclical fuel

costs, usage versus capacity, and competitive pressures on airfares.

9. Energy

This category includes large integrated international companies, domestic exploration companies, and energy

services companies. Each industry has its own dynamics, but ultimately all are driven by the supply and demand

picture for energy worldwide. Political events have historically had a major impact on these industries. Stocks tend to

be popular with investors late in the business cycle.

10. Utilities

Electric companies have historically been very sensitive to interest rates because of the large debt financing costs they

must incur in order to build their infrastructures. These stocks tend to perform well in an environment of declining

interest rates. Telephone companies may offer attractive long-term growth opportunities, as they diversify and compete

in recently deregulated telecommunications markets.

11. Precious Metals

Precious metals and the stocks of companies that mine and process them can be affected by industrial and consumer

demand, but the largest factor contributing to volatility in this category is generally inflationary pressure. Investors often

flock to this category late in the expansion cycle.

| |

| |

| |

| |

| |

| |